Banking the Unbanked

Powering global financial inclusion

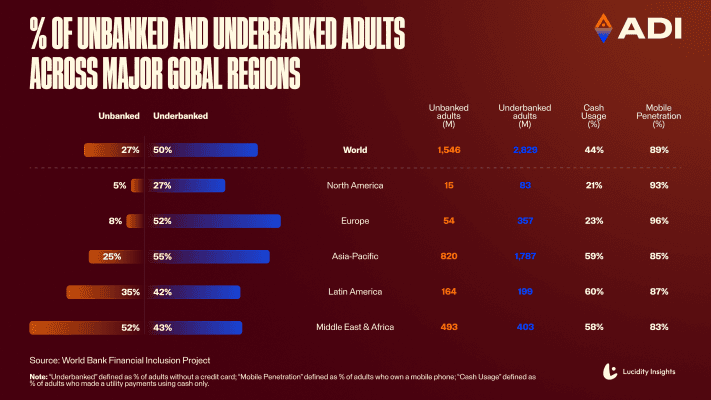

A major constraint on the financial growth of emerging markets is the limited access to secure banking and financial services. As a result, a large portion of their populations tend to be “unbanked,” which means they don’t have access to traditional banking services. In many cases, unbanked populations must rely on transacting via cash, checks, or prepaid cards.

While the internet has transformed the financial landscape for a majority of people in certain regions, an estimated 1.4 billion people around the world remain unbanked. In fact, recent data shows that a total of 45 countries had larger unbanked populations than banked. Many of these countries are in regions such as the Middle East, Africa, and Latin America, which are the largest unbanked markets in the world:

In addition to limited access to financial services, another problem faced by many unbanked countries is rooted in their local currencies, which face fragmentation, illiquidity, and inflation. As a result, demand outside the currency’s native country is very low, and the high fees and large spreads in forex markets are unaffordable for many individuals and local businesses.

Stablecoins have proven to be a viable solution to these issues, and there’s clear evidence that demand is strong. For example, stablecoin-based remittances have become one of the largest global use cases for web3, now accounting for 15% of total stablecoin volume. And adoption across Asia and Africa accounts for almost half of global stablecoin volume, showing increased popularity in areas with limited access to banking services.

This demonstrates that people value their low-cost, fast infrastructure as well as price reliability enough to shift from legacy payment networks onto blockchain rails. However, there’s still significant room for growth.

Just as many individuals in emerging markets face barriers to financial inclusion, there are also hurdles to achieving widespread stablecoin adoption. Many individuals and local businesses still lack access to the financial services necessary to use them to their full potential. Without access to traditional financial services such as online banking, there’s no simple way for people to access Web3 services via “on ramps,” which are platforms that enable users to exchange their fiat currency for stablecoins or other digital assets.

ADI is here to solve these issues by bringing unified, onchain financial infrastructure to one billion people around the world – starting with regions across the Middle East, Africa, and Asia.

The solution: Accelerating adoption with onchain financial rails

While these emerging markets are certainly plagued by hurdles to financial inclusion, there are two major tailwinds which can fuel adoption:

- Our core target regions show some of the highest demand for stablecoins in the world.

- Regional demographics are favorable for digital asset adoption.

Many unbanked regions have robust population growth as well as young demographics. For example, MENA (Middle East and North Africa) countries are home to over 500 million people with a median age of 26.8. With over 80% mobile penetration, the MENA region is full of young, tech-savvy individuals who are open to digital financial solutions.

This is also evident by the increasing trend of individuals using mobile services as a replacement for traditional banking; between 2021 and 2024, MENA and Sub-Saharan Africa experienced a nearly-10% increase in financial account ownership due to mobile technology.

Our mission at ADI is to create awareness and adoption of onchain financial services in these regions, and ultimately play a leading role in banking the unbanked. In order to make this a reality, ADI is creating compliant and highly-performant payment rails targeting adoption at the enterprise and government levels, enabling client and local populations to be easily and efficiently onboarded.

We’re building ADI Chain, a chain dedicated to bringing payments onchain, improving settlement times, and integrating mobile-first financial rails. Better cross-border finance will make for a more empowered citizenry — one that can fully participate in the global economy, regardless of geography or background.